What is the Asia Pacific Wet Pet Food Market Overview – Definition, scope, and significance?

The Asia Pacific Wet Pet Food Market comprises ready‑to‑serve, moisture‑rich dietary products formulated for companion animals, primarily dogs and cats, sold in cans, pouches, and other sealed containers. The market’s scope includes all product categories, packaging formats, and distribution channels—from supermarkets to online platforms—across the entire Asia Pacific region. Its significance stems from rising pet ownership, evolving human‑like attitudes toward pets, and increasing disposable income, which collectively drive demand for convenient, nutritionally balanced wet foods that complement dry kibble diets.

What are the Asia Pacific Wet Pet Food Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include growing urbanization, higher pet humanization, and preference for premium nutrition that wet food offers. Restraints arise from price sensitivity in emerging economies and limited cold‑chain infrastructure for certain packaging. Challenges involve intense competition from established dry‑food brands and regulatory variations across countries. Opportunities are evident in product innovation (e.g., high‑protein, grain‑free formulas), expansion of e‑commerce channels, and development of sustainable packaging such as recyclable pouches.

What are the Asia Pacific Wet Pet Food Market Growth Trends?

Current trends feature a shift toward single‑serve, portion‑controlled pouches that cater to busy pet owners. Brands are launching limited‑edition, locally inspired flavors to attract regional palates. There is a noticeable rise in premium and functional wet foods fortified with probiotics, antioxidants, and joint‑support compounds. Additionally, the market is witnessing a convergence of wet and dry formats, with hybrid offerings that combine the convenience of wet meals with the shelf stability of dry products.

How has COVID‑19 impacted the Asia Pacific Wet Pet Food Market and what is the recovery trajectory?

The pandemic accelerated online grocery adoption, boosting wet pet food sales through digital platforms as consumers sought home delivery. Initial supply‑chain disruptions caused temporary stock shortages, but strong brand loyalty facilitated a rapid rebound. Post‑COVID, the market is on a steady recovery path, with e‑commerce now accounting for a larger share of total sales and consumer confidence in pet nutrition remaining robust.

What does the Asia Pacific Wet Pet Food Market Competitive Landscape look like?

The competitive arena is characterized by a mix of multinational giants and regional specialists. Leading players such as Mars, Incorporated and Nestlé leverage extensive distribution networks, while companies like De Haan Petfood and FirstMate Pet Foods focus on niche, high‑quality formulations. Recent consolidation includes strategic partnerships and acquisitions aimed at expanding product portfolios and penetrating new channels, particularly online.

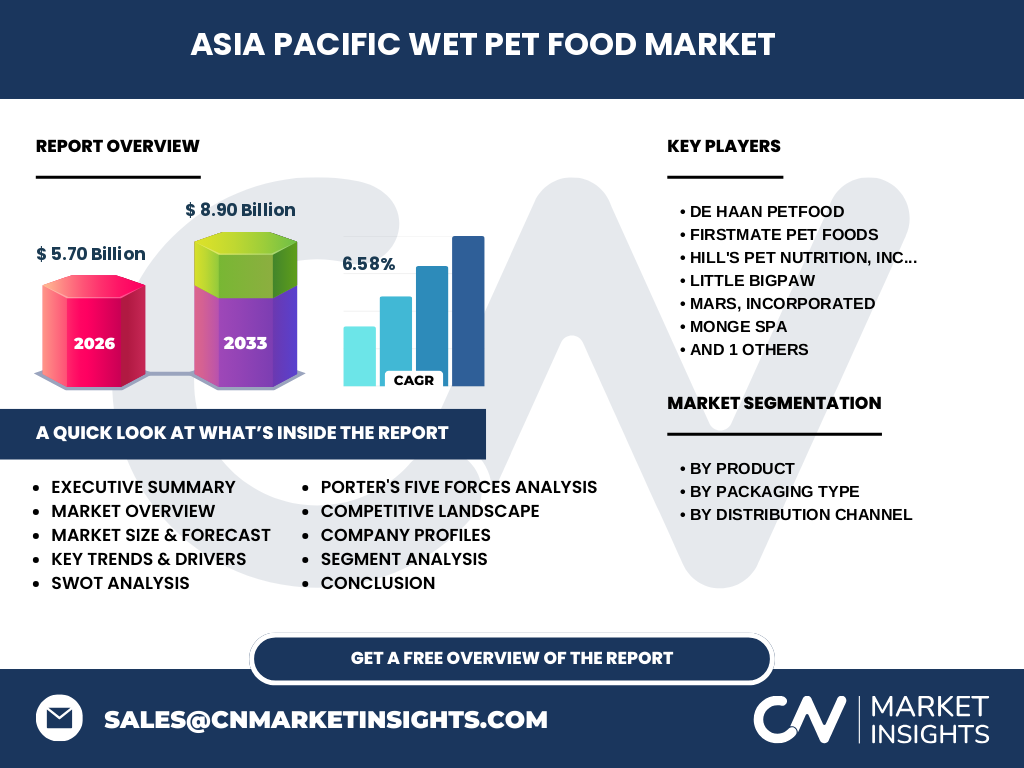

What are the key findings in the Executive Summary of the Asia Pacific Wet Pet Food Market?

The market is valued at US$5.70 billion in 2026 and is projected to reach US$8.90 billion by 2033, reflecting a CAGR of 6.58 %. Growth is propelled by pet humanization, premiumization, and digital sales channels. Dog wet food leads the segment, followed by cat wet food. Canned packaging retains dominance, yet pouches are gaining traction due to convenience. The region’s most dynamic markets are China, Japan, and Australia, where consumer spending on pet nutrition is highest.

What is the forecast for the Asia Pacific Wet Pet Food Market for 2025‑2032?

Building on the 6.58 % CAGR, the market is expected to sustain steady expansion through 2032, with annual growth driven by rising middle‑class populations and increasing pet adoption rates. Innovation in functional ingredients and environmentally friendly packaging will further stimulate demand, while digital retailing will enhance market reach, especially in tier‑2 and tier‑3 cities.

How is the Asia Pacific Wet Pet Food Market sized and shared by segmentation?

By product, dog wet food commands the larger share, reflecting higher consumption volumes compared with cat wet food. Packaging segmentation shows canned formats still leading due to established shelf‑life advantages, but pouches are rapidly gaining market share thanks to portability and reduced waste. Distribution‑channel analysis reveals supermarkets and hypermarkets as the primary sales outlet, while specialized pet shops and online channels together contribute a growing minority, with e‑commerce accelerating its share year over year.

What is the Global Asia Pacific Wet Pet Food Market Size and Share by Region?

The Asia Pacific region accounts for the majority of global wet pet food consumption, anchored by populous markets such as China, Japan, South Korea, and Australia. While exact regional split figures are not disclosed, the region’s aggregate valuation of US$5.70 billion in 2026 underscores its leadership position relative to other continents.

What does the Regional Analysis of the Asia Pacific Wet Pet Food Market reveal?

China exhibits the fastest growth trajectory, driven by urban pet owners seeking premium nutrition. Japan remains a mature market with stable demand and a strong preference for high‑quality canned foods. Southeast Asian nations like Indonesia and Vietnam present emerging opportunities as pet ownership rises and retail infrastructure improves. Australia shows a high per‑capita spend on pet food, with a notable shift toward sustainable packaging.

Who are the leading companies in the Asia Pacific Wet Pet Food Market and what are their strategies?

Key players include De Haan Petfood, FirstMate Pet Foods, Hill’s Pet Nutrition, Inc., Little BigPaw, Mars, Incorporated, Monge SPA, and Nestlé. Strategies revolve around product line extensions into grain‑free and functional wet foods, investment in local manufacturing to reduce logistics costs, and expansion of direct‑to‑consumer platforms. Partnerships with veterinary experts and collaborations with influencers are also employed to enhance brand credibility.

What does Porter’s Five Forces analysis indicate for the Asia Pacific Wet Pet Food Market?

• Threat of new entrants: Moderate, due to high capital requirements for production and regulatory compliance.

• Bargaining power of suppliers: Low to moderate, as raw‑material sources are diversified and many manufacturers secure long‑term contracts.

• Bargaining power of buyers: Increasing, given consumers’ access to information and alternative brands, especially online.

• Threat of substitutes: Moderate, with dry food and fresh‑prepared pet meals offering alternatives.

• Competitive rivalry: High, driven by numerous multinational and local brands competing on price, quality, and innovation.

What are the SWOT analysis highlights for the Asia Pacific Wet Pet Food Market?

Strengths: Robust growth drivers, expanding middle class, and strong brand loyalty.

Weaknesses: Price sensitivity in lower‑income segments and limited refrigeration infrastructure for certain products.

Opportunities: Innovation in functional ingredients, sustainable packaging, and digital sales channels.

Threats: Regulatory changes, supply‑chain disruptions, and intensifying competition from both dry and fresh pet‑food sectors.

How does the value chain of the Asia Pacific Wet Pet Food Market operate?

The value chain starts with raw‑material sourcing (meat, vegetables, additives), followed by formulation and processing (cooking, aseptic sealing). Packaging manufacturers supply cans and pouches, after which products are distributed to wholesalers, retailers, and e‑commerce fulfillment centers. End‑customers purchase through brick‑and‑mortar outlets or online platforms, with after‑sales support and pet‑nutrition counseling provided by brand representatives.

What key investment insights can be drawn for the Asia Pacific Wet Pet Food Market?

Investors should target brands with strong e‑commerce capabilities and those developing sustainable packaging, as these areas align with consumer trends. Partnerships with local manufacturers can mitigate supply‑chain risks and lower cost structures. Moreover, allocating capital toward functional wet foods—such as high‑protein or joint‑health formulas—offers premium pricing potential and market differentiation.

What conclusions can be drawn from the Asia Pacific Wet Pet Food Market analysis?

The market is on a solid growth path, underpinned by pet humanization and rising disposable incomes. While price sensitivity and regulatory complexities pose challenges, opportunities in product innovation, digital distribution, and eco‑friendly packaging are compelling. Companies that adapt quickly to these dynamics are likely to capture the expanding share of the US$8.90 billion market projected for 2033.

What research methodology was used for this market study?

The study employed a mixed‑method approach, combining primary interviews with industry experts, distributors, and pet‑owner focus groups, alongside secondary data collection from company reports, trade publications, and governmental statistics. Quantitative analysis utilized CAGR calculations and market sizing based on the provided baseline of US$5.70 billion (2026) and forecast of US$8.90 billion (2027‑2033). Qualitative insights were synthesized to identify trends, drivers, and competitive dynamics.

What is the scope of this research and its limitations?

The scope covers the full Asia Pacific region, addressing product, packaging, and distribution segmentation, and includes analysis of major competitors and market forces. Limitations stem from the reliance on publicly available data and the exclusion of proprietary financial figures beyond the provided market size and growth rates. The study does not detail country‑specific market shares due to data constraints.

Which key companies and recent developments are notable in the Asia Pacific Wet Pet Food Market?

Prominent firms such as De Haan Petfood, FirstMate Pet Foods, Hill’s Pet Nutrition, Little BigPaw, Mars, Incorporated, Monge SPA, and Nestlé have announced new product launches focusing on grain‑free and high‑protein wet formulas. Recent developments include Mars’ acquisition of a regional wet‑food producer to enhance its portfolio, Nestlé’s rollout of recyclable pouch packaging in Japan, and Hill’s partnership with veterinary clinics in Australia to promote clinical nutrition lines. These activities underscore a market shift toward premiumization and sustainability.